Editor’s Note: With summer in full swing, many of the practitioners in the accounts payable world are taking vacations ahead of the crush of the fall months. In honor of that, the team here at Payables Place is inaugurating its “Summer Rewind” series with a pair of our favorite posts from roughly a year ago. Today, we are re-running the examination of Apple Pay and its possibility as the killer app for mobile payments, which originally ran in September 2014.

Apple (NASDAQ: AAPL) has a habit of taking aim at industries it decides are antiquated. Thirteen years ago it was the way consumers purchased music; on September 9, the Silicon Valley giant decided that mobile payments deserved its attention.

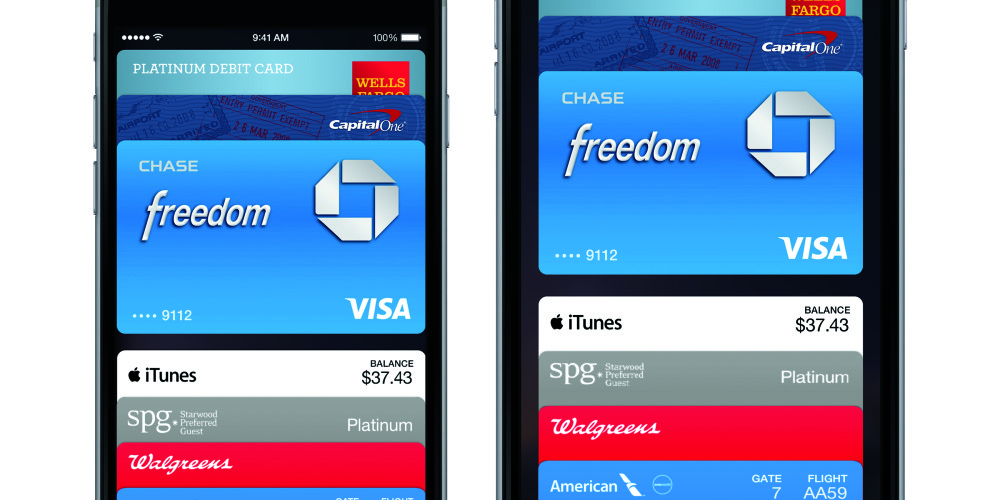

That fateful Tuesday, Apple unveiled “Apple Pay,” a mobile-payments app that uses Near Field Communication (NFC) technology to allow iPhone 6 and 6 Plus users to pay with their cell phone at terminals enabled with the right software. To keep payments secure, the app uses a combination of fingerprinting and tokenization—creating essentially a virtual credit card so the consumer’s real credit card number is never seen or stored by the merchant.

Apple Pay boasts partnerships with card companies American Express, Master Card, and Visa as well as JPMorgan Chase, Bank of America, Citi, Wells Fargo, and Capital One on the banking side of the fence. The app is decidedly business-to-consumer in focus, but payment technology providers such as Stripe (known for its APIs that enable web-based payments) already have documentation that allows developers to integrate Apple Pay into their applications.

Perhaps the most interesting part about this new solution, however, is that Apple Pay doesn’t process the payment itself. Rather, all the app does is secure the consumer’s personally identifiable information and then pass it along to the credit card issuer and/or bank for payment processing. This is in direct contrast with the approach take by PayPal, which does end-to-end payment processing.

“Security and privacy is at the core of Apple Pay. When you’re using Apple Pay in a store, restaurant, or other merchant, cashiers will no longer see your name, credit card number, or security code, helping to reduce the potential for fraud,” said Eddy Cue, Apple’s senior vice president of Internet Software and Services, in a statement announcing the product’s release. “Apple doesn’t collect your purchase history, so we don’t know what you bought, where you bought it or how much you paid for it. And if your iPhone is lost or stolen, you can use Find My iPhone to quickly suspend payments from that device.”

News reports from The Financial Times also detail that Apple receives 15 cents out of every $100 transaction as its portion of the credit-card interchange fee. Clearly, payment providers are banking on the app causing a corresponding increase in credit card payments so they make more money overall. A 0.15% fee is small potatoes to pay for growth in revenue from more interchange fees.

With this clearly being a consumer solution, one has to wonder what Apple Pay means for business-to-business mobile payments.

Apple Pay is not a new idea. NFC payment technology has existed for quite some time, and worked well for at least the last five years. The problem is that mobile payments don’t have great adoption rates in the United States—particularly when looking at general-use applications and not something store-specific (store-specific apps have seen some deep success; Starbucks and Dunkin Donuts are two examples). Apple is unique in that Apple Pay will come essentially pre-loaded on all new iPhones. This means that all a consumer needs in order to use the app is an iTunes account with a credit/debit card attached, and a merchant with an NFC-enabled credit card terminal.

I could see this becoming another killer app in the Apple toolshed. Consumer technology also has a tendency to bleed over into the business world—take social media tools, for example—and Apple Pay could be yet another case where this happens. There is an almost immediate applicability for commercial cards here; small business owners or sole proprietors could simply photograph a company credit card into the app, and instantly receive a tokenized, secure payment method for one-off business expenses. Larger enterprises could craft a corporate iTunes account and add multiple users as well as corporate cards (and associated limits) into the system.

More to the point, by taking aim solely at plastic credit cards and not at the underlying payment ecosystem, Apple has managed the impressive feat of altering a process without alienating the established players in the space. This is in contrast to companies like PayPal that tried to take an end-run around other payment providers.

In the short term, it’s unlikely that Apple Pay will make many inroads beyond the consumer purchase world. What’s truly likely to happen is solution providers see what Apple’s done and try to mimic the procedure for B2B mobile payments. Companies such as Ariba and Basware already have invested in electronic payment solutions (with different approaches mind you) and this isn’t even considering the numerous B2B payment solution providers like Syncada (from U.S. Bank), 3 Delta Systems, or Traxpay that already exist.

So while Apple Pay may become a killer app for the business-to-consumer mobile payments world, it’s unlikely that there will be any impact on the B2B mobile payments ecosystem in the near-term. That said, never bet against a company that’s run by a former Chief Procurement Officer.

Check out these related articles for more:

How ePayments Address Collaboration Concerns

How ePayments Address Resource Concerns

AP Predictions for 2015: B2B Payments Become a Strategic Business Process

Comments are closed.